Blog • November 27, 2025 - Jaran Mellerud

Certain hosting bros are very creative when it comes to crafting cool narratives to convince people to buy more mining machines. One of the most aggressively pushed — and misunderstood — is the idea that bitcoin mining is a fantastic tax strategy that can significantly reduce your taxes.

It sounds compelling: buy miners, use bonus depreciation, and eliminate your tax bill.

And if you only hear the marketing version, it can seem straightforward.

To examine whether this claim holds up, we modeled three tax strategies for a person earning $1 million in taxable income and compared their tax outcomes over a 10-year period. Each strategy uses the same assumptions to allow for an apples-to-apples comparison.

We simulated three tax strategies for a person with $1 million in pre-mining taxable income.

The investor uses his entire $1 million to buy mining machines and takes 100% bonus depreciation in year one.

The investor again buys machines in year one, but then reinvests all mining cash flow and his $1 million pre-mining taxable income into new miners for the next three years, taking bonus depreciation each time.

Some promoters claim you can roll this over indefinitely, but doing so would require exponentially increasing CapEx and being forced to buy machines in all market conditions — something that is not practically feasible.

The investor simply accepts the tax bill in year one and uses the remaining cash to buy BTC. He can also buy other passive investments, like stocks or gold.

To isolate tax effects — not mining economics — we use the following assumptions:

These assumptions allow us to isolate the tax effects of each strategy without letting mining volatility or BTC performance distort the comparison.

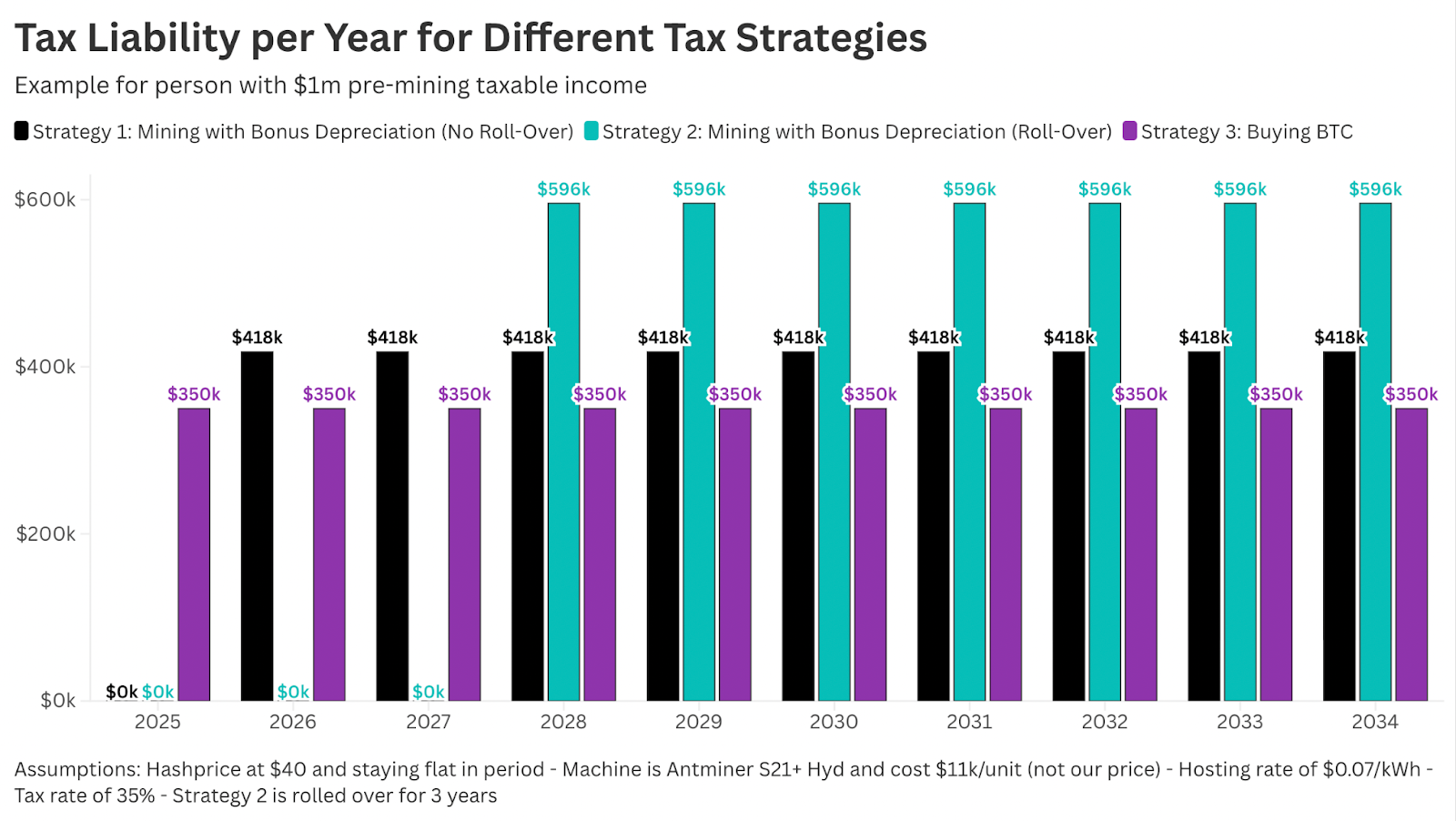

We will now compare the annual tax liability of the three different strategies for ten years.

Strategy 1 eliminates taxes in year one, but once depreciation is gone, mining produces taxable profit every following year. The tax bill rises steadily because there are no depreciation offsets left.

Strategy 2 eliminates taxes for three years due to continuous reinvestment and bonus depreciation, but when reinvestment stops in year four, taxes surge sharply because the mining operation is now much larger and produces more taxable income.

Strategy 3 results in consistent tax liability every year. The investor pays tax in year one, but because there is no mining income, later years have no additional taxable income from mining.

Bonus depreciation doesn’t reduce taxes — it only delays them. And once depreciation disappears, mining dramatically increases taxable income.

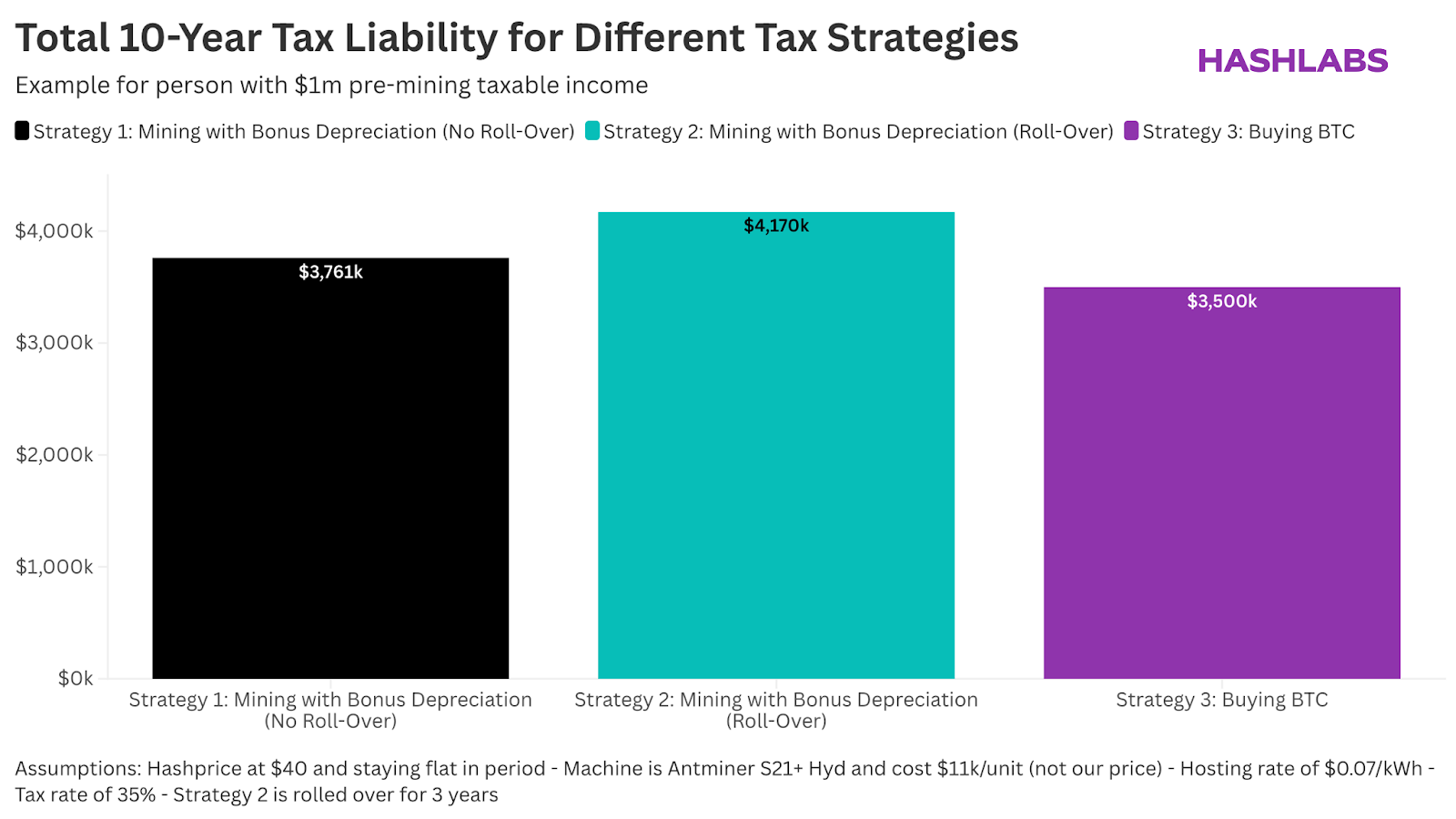

We will now compare the accumulated tax burden over 10 years for the different tax strategies.

Strategy 1 ends up with a higher accumulated tax bill because years 2–10 generate taxable mining profit that more than offsets the year-one tax elimination.

Strategy 2 also leads to a higher total tax burden, even though early-year taxes are zero. The large mining footprint built through reinvestment produces large taxable income later.

Strategy 3 has the lowest total tax burden since passive bitcoin ownership does not generate taxable income each year.

Mining creates ongoing taxable income, so total income taxes end up higher than if you simply bought bitcoin.

From our analysis so far, it is clear that mining with bonus depreciation can reduce your tax bill in the short-term, but will ultimately increase your long-term tax bill. It simply shifts the tax obligation into later years (and creates even more taxable income).

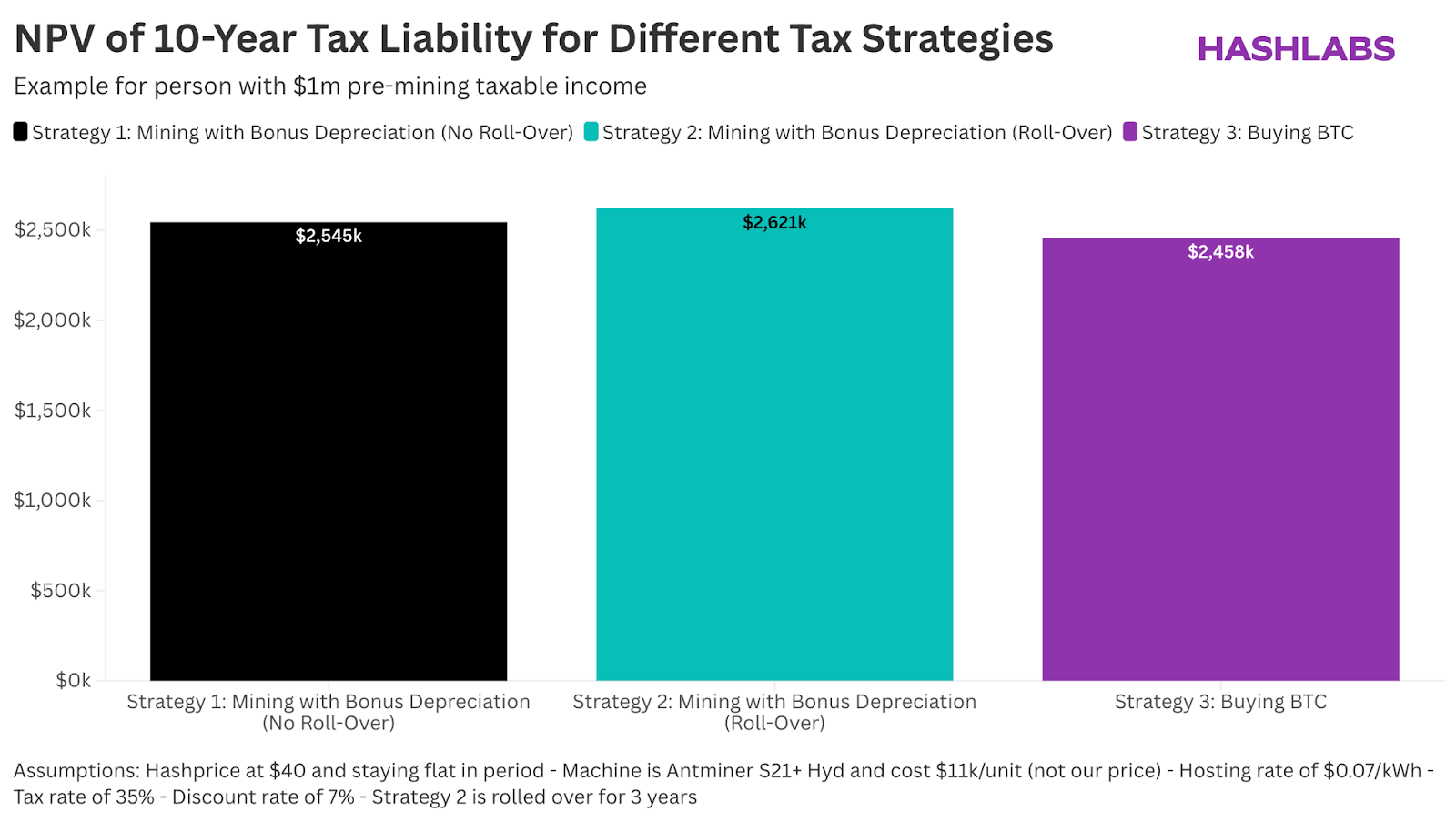

Then, the ultimate question for our analysis is - does the time value benefit of paying taxes later make up for the higher long-term tax liability caused by the mining activities?

The answer is no. As you can see on the chart below, both the bonus depreciation strategies actually increase the net present value (NPV) of your 10-year tax liability.

Strategy 1 produces a high NPV tax liability, because the year-one benefit is overshadowed by nine years of taxable mining income.

Strategy 2 looks even worse. The high taxes from year 4 onwards, when the investor cannot keep up with the forced reinvestment scheme, creates a very high NPV tax liability.

Strategy 3 has a lower NPV of taxes than Strategy 1 and 2, despite paying taxes in year one, because there is no recurring mining income to tax.

Even when discounting future payments, mining strategies do not produce meaningful tax savings — it actually leads to a higher tax NPV.

And before the hosting bros start: no, you cannot use a 30% discount rate on a tax bill. Mining cash flows are risky; tax cash flows are certain. You don’t gamble with the money you need to pay the IRS. Even 7% is generous when Treasuries are ~4%. Using a high-risk discount rate on a guaranteed obligation isn’t smart — it’s basic financial misunderstanding.

Norway went through almost the exact same phenomenon during the kommandittselskap (K/S) shipping boom of the 1970s–1990s. Back then, shipping brokers aggressively pushed investment structures built around accelerated depreciation. The pitch was nearly identical to what today’s hosting bros are saying about bonus depreciation in mining: “Put money in now, wipe out your taxes, reinvest again next year, and keep rolling it forward.”

It sounded clever, it looked tax-efficient, and it was marketed with absolute conviction.

Oil tanker

But here’s what actually happened: the only people who consistently made money were the brokers selling the ships.

Most investors were trapped in a cycle of forced reinvestment, buying more and more vessels — often in terrible market conditions — just to maintain the tax benefits. When the reinvestment treadmill stopped, tax bills surged, asset values collapsed, and the majority of investors lost money.

This is why K/S structures in Norway became a cautionary tale: tax benefits became a smokescreen for poor underlying investments.

Be extremely wary when someone is trying to sell you something and spends most of their pitch talking about tax benefits (or other vague side perks) rather than the only thing that actually matters in investing: real, risk-adjusted returns.

Tax structures can easily hide bad economics — and in the K/S boom in Norway, that’s exactly what happened.

Trying to engineer clever tax maneuvers typically leads to:

If your goal is truly to reduce taxes, the only real solution is to move yourself or your business to a low-tax jurisdiction (consistent with CFC rules and residency requirements).

A tax strategy that forces bad investment decisions is worse than no tax strategy at all.

Thinking that mining with bonus depreciation will reduce your long-term taxes is a bit like peeing in your pants to stay warm. It feels good right now, but you end up colder later.

Mining increases long-term taxes because it generates taxable income every year. Bonus depreciation simply shifts the tax burden to later — it never removes it.

If you want to mine, great. Use bonus depreciation. But don’t mine because of bonus depreciation. It’s not a tax strategy. It’s just a timing shift, and a misleading one.

Here is a link to the Google Sheet with all the assumptions. Feel free to duplicate this sheet and play around with it.

Share the article with friends and subscribe to our newsletter if you found it valuable.