Blog • December 2, 2025 - Valentin Rousseau

This new research report, divided into two parts, deals with a long-standing topic of interest in the industry: the necessary but detrimental cost of shareholder dilution in a capex-intensive industry. This article is the genesis on a wider research assessing miners strategies by comparing the cost of dilution to the bitcoin value per share produced.

This first part introduces the historical financing landscape within the industry since January 2022, distinguishing debt, convertible notes and equity proceeds supporting hashrate expansion. Acting as a key pillar for the second part, we estimated a mean $/TH on ASICs annual purchases.

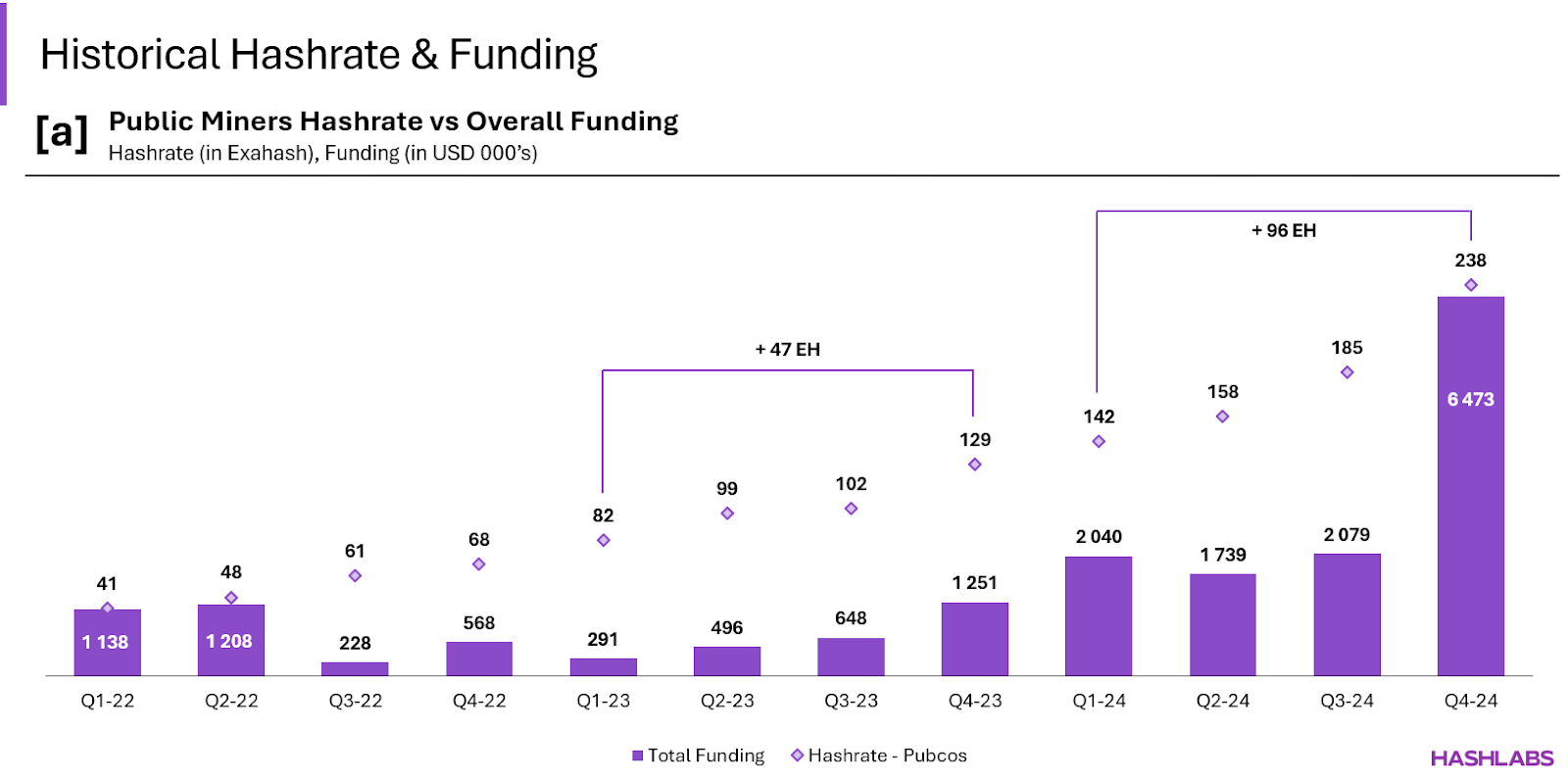

Since their public introductions via IPO, SPAC or related public introductions, current Bitcoin miners have experienced a cycling environment from 2022 bear market to 2024 halving and 2025 resurgence. The following data displayed are based on a sample of 18 miners averaging a 27.1% share of the network from Q1-22 to Q3-25.

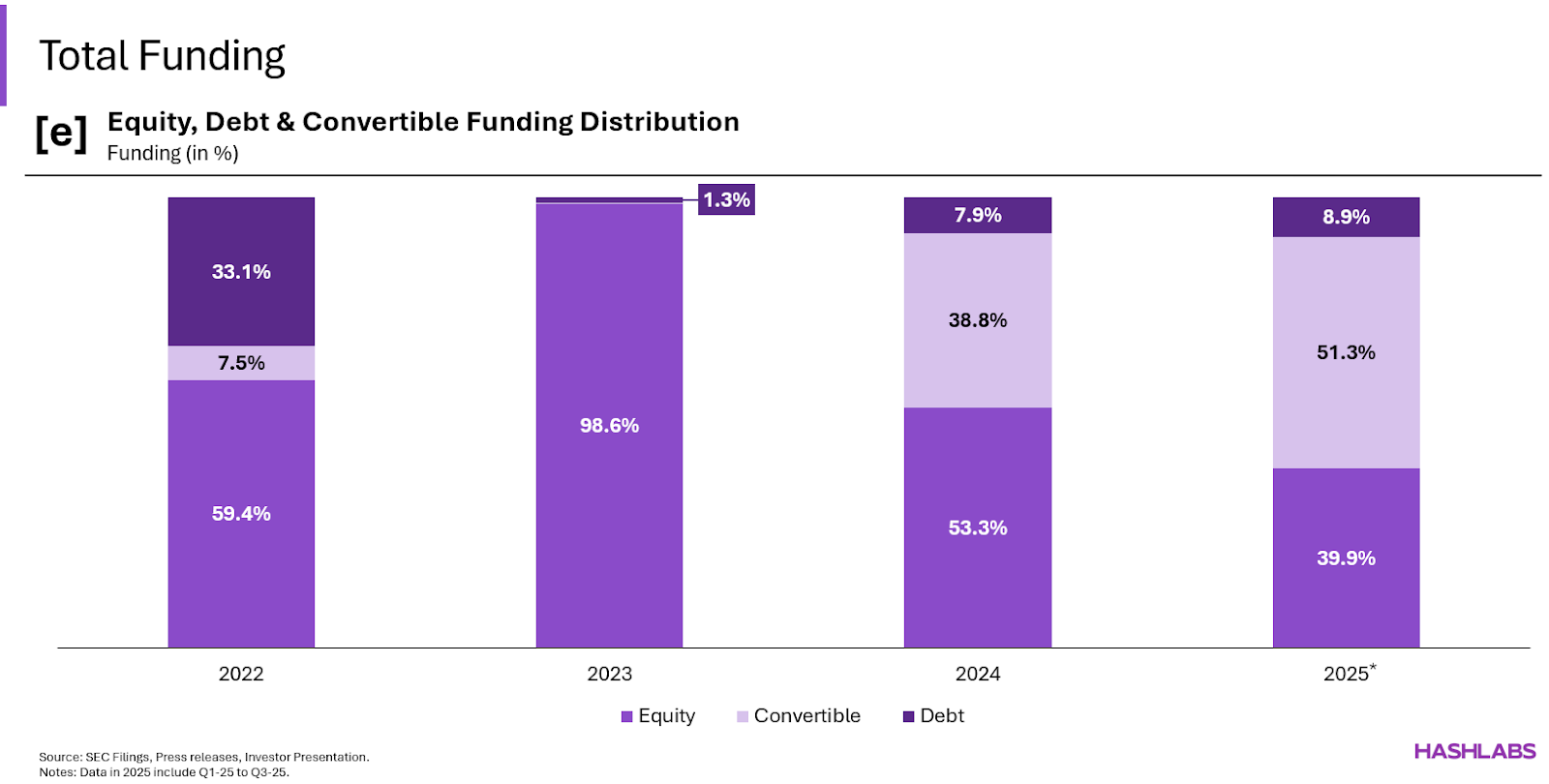

Ordering a massive amount of S19 generation in 2021 to fuel their scaling appetite, with a price peaking at $119/TH, miners irremediably faced a first hurdle: supply chain bottlenecks. This overzealous market took an end in Q3-22 with much more modest proceeds from debt and equity. In total, $2.4 billion were raised during H1-2022 against only $1.6 billion from Q3-22 to Q2-23. Despite frivolous capital markets, previous ASIC orders scaled public miners’ operations bringing more exahash online in 2022 and 2023, with a hashrate jumping from 41 EH in Q1-22 to 102 EH by Q3-23.

Afterwards, as the ASIC supply loosened and economics improved, miners raised record amounts, especially in 2024 reporting $12.3 billion against only $2.7 billion a year ago. In 2024, Public companies energized 96 EH, a strong rebound from previous year incremental hashrate at 47 EH. Nevertheless, the discrepancy between the level of capital raised between 2023 and 2024 is too important to explain the 48 EH gap.

On the ASIC market front, after the substantial drawdown underwent since December 2021 machines price started to plateau in mid-2023, implying 2024 additional public miners’ hashrate would have been higher at such discounted prices.

Key factors explaining the discrepancy between capital inflows and hashrate energization:

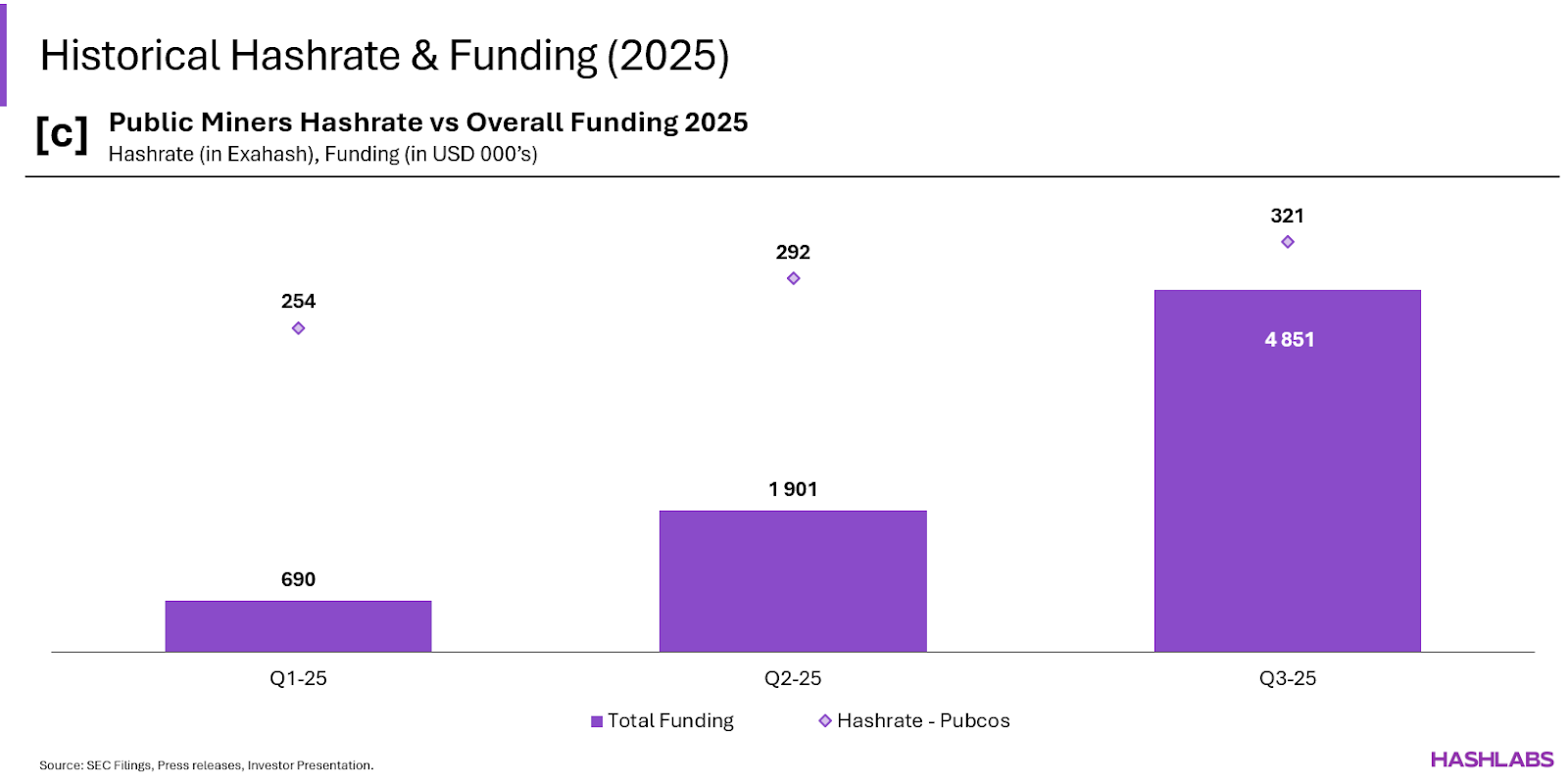

In 2025, the HPC conversion not only marked a strategic expansion, but signaled a departure from miners’ core business model. A growing number of Pubcos are claiming a complete or significant divestiture of their bitcoin mining segment for the coming years.

Chiefly, the sudden spike in proceeds from $0.7 billion at Q1 to $4.9 billion at Q3-25 outlines this pivot. As miners secured a wave of HPC deals to fuel the hyperscalers’ appetite, a tremendous injection of capital followed with a record of convertibles notes issuance to cover the massive infrastructure CAPEX requirements.

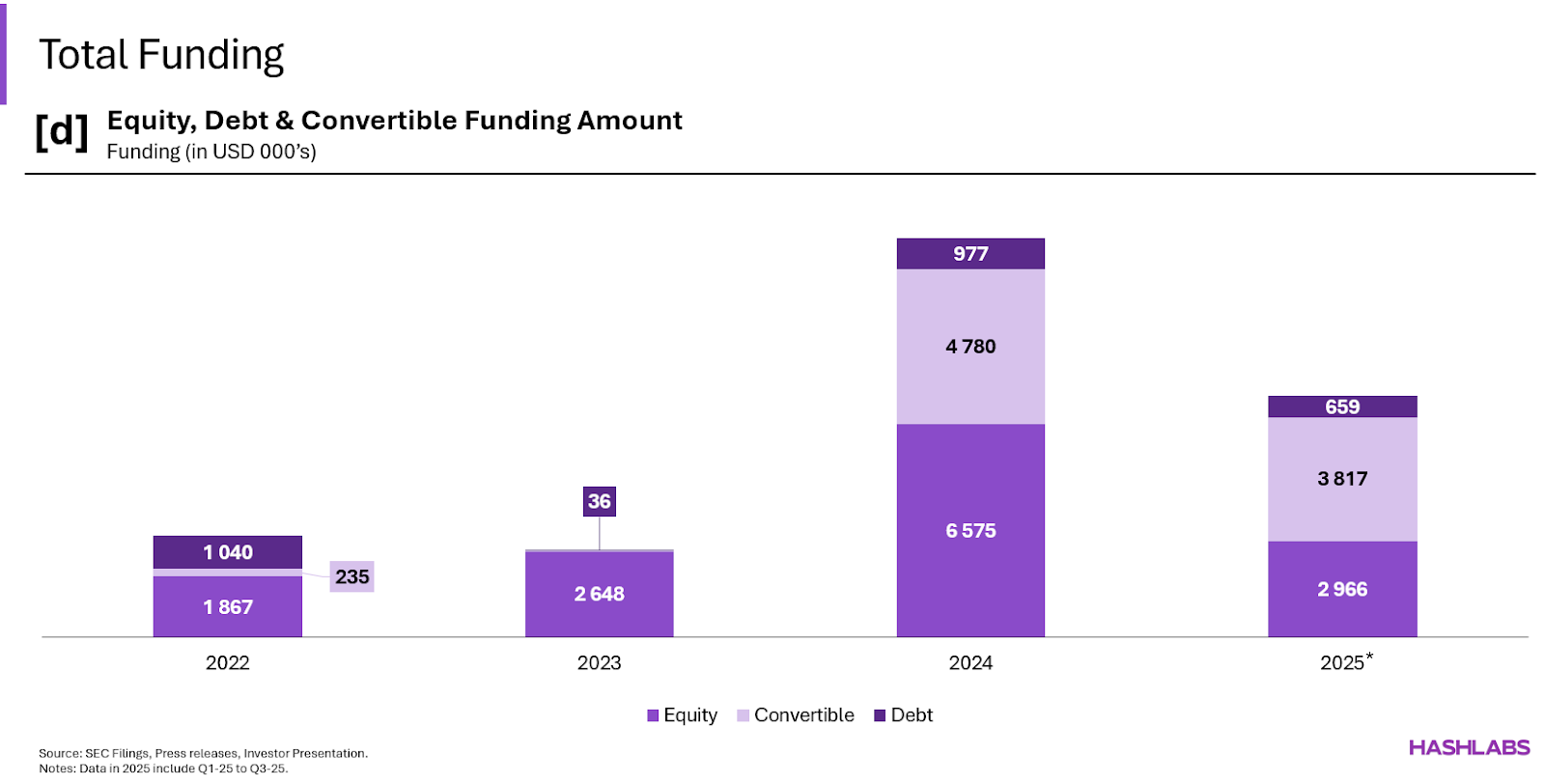

At his acme debt reached 47.9% of the total amount raised (in Q4-2022) with $1.0 billion for the whole year of 2022 against only $0.1 billion from Q1-2023 to Q3-2024 and $1.6 billion since Q4-2024. The devastating impact of 2022 crypto winter, with miners trapped under mountains of debt, had rippled effects on debt markets where traditional ASIC-backed loan almost disappeared and the rise of interest rates made debt unsustainable for the high risk-profile of Bitcoin mining operations.

Crunched for capital, miners that wanted to survive or capitalize on opportunities had very few options at hand expect dilution. The supremacy of equity in the fundraising structure became particularly prevalent in 2023, with nearly 98.6% all of the proceeds coming from this source. In 2024, equity issuances dominated the capital stack but at a much lower weigh accounting for 53.3% of total proceeds versus 38.8% for convertibles. Notes eventually reversed the dominance in 2025 becoming king with 51.3%1 of the total capital structure.

At the end of the day, from Q1-22 to Q4-24, the equity play and convertible issuance resulted from either:

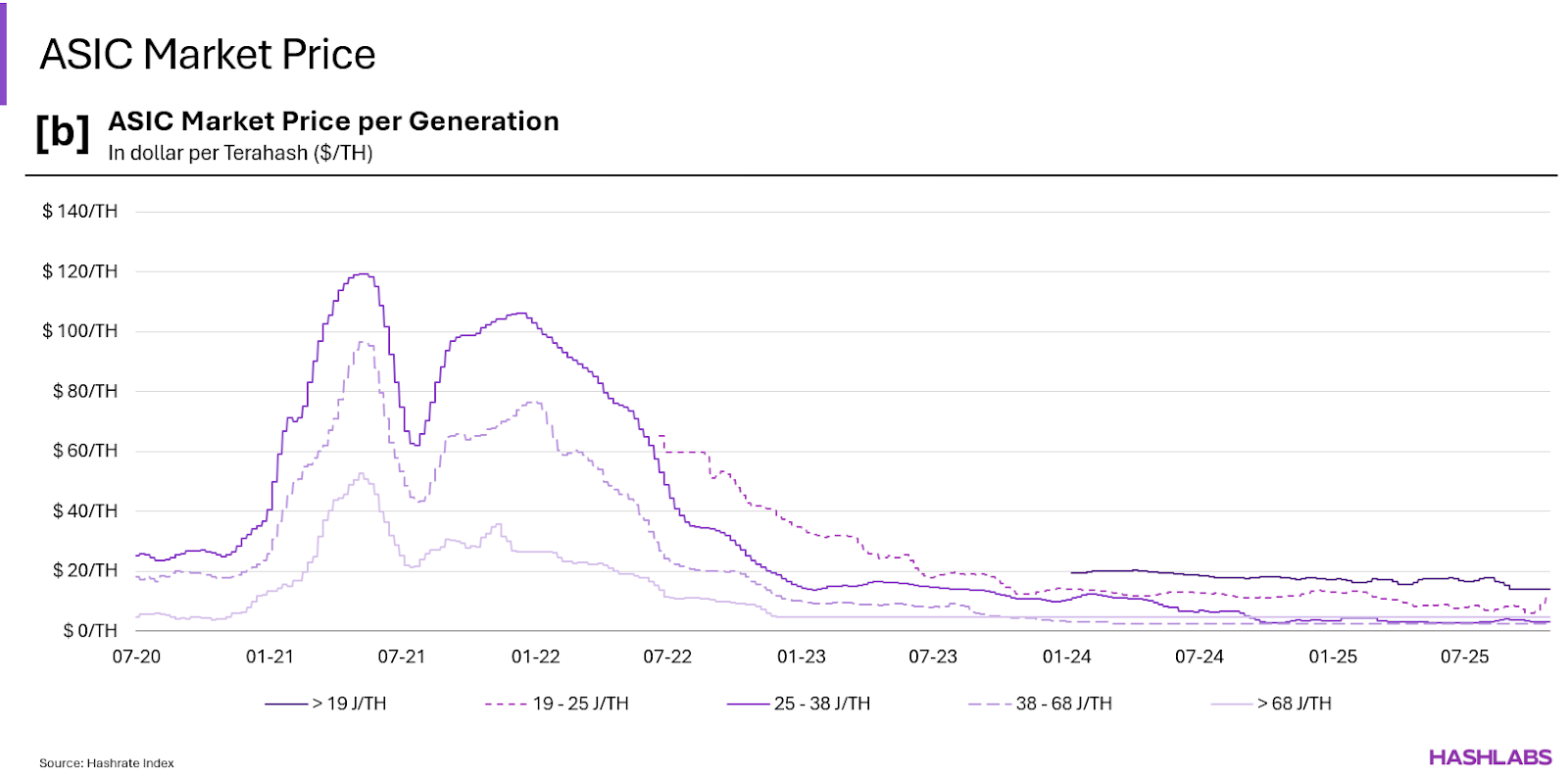

As the ultimate goal of this article is to pave way for the comparison between the cost of dilution and the value of the bitcoin produced, we first looked at the machine CAPEX shedding light on miners’ ability, or not, to time the volatile ASIC market.

Importantly, the estimated $/TH spent annually is an approximation and is based on a restricted sample of 8 public miners: Bitfarms, Cipher, CleanSpark, DMG, Hive, IREN, MARA and Riot. To compute the estimated $/TH spent annually, we calculated the incremental annual capex in the PPE for mining rigs. Then this amount was divided by the hashrate energized over the year. One should be aware of a limitation of this approach: potential disposals (when undisclosed) of machines might skew the quantification of actual PPE added over the year.

From the results obtained we observed a mean $24.9/TH in 2023, with a maximum at $32.3/TH and a minimum at $19.0/TH. Based on ASIC Price index data from Luxor 19J/TH to 25J/TH machines started the year at $34.2/TH and ended at $14.2/TH.

In 2024, ASIC prices wind down at much lower pace with a new generation (15J/TH to 19J/TH) ranging from $20.3/TH to $17.2/TH. By contrast our sample estimates the maximum amount spent per TH reaches $29.6, possibly skewed by disposals or previous payables of 2023 orders entering the PPE in the 2024 EOY balance sheet. The lowest point at $15.5/TH seems more credible with potential acquisitions of mid-gen models (19J/TH to 25J/TH) at discounted prices.

Equity will remain a powerful and central to miner strategy, but it seems that it will be used with more precaution as shareholders might expect outperformance over Bitcoin in bull markets. However, to keep fulling their business with fresh money while allowing a gradual BTC strategy accumulation or to diversify their business, alternatives financing will become central.